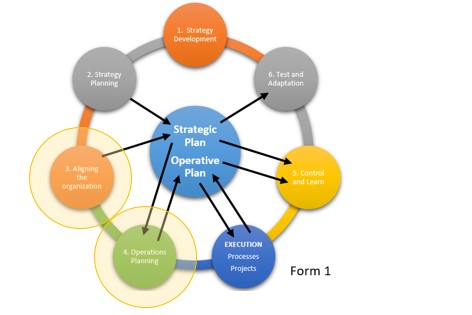

Based on the Execution Premium methodology of Kaplan and Norton, a comprehensive and integrated management system is formulated that explicitly relates the formulation and planning of the strategy. We can refer to Form 1.

Aligning the organization with the Strategy

To capture the full benefits of an organization with multiple businesses and functions, executives should relate the company’s strategy to the strategies of its individual business and functional units, and align and motivate employees. At this stage, companies must answer three questions:

1. How can we make sure that all business units are aligned? The strategy is usually defined at the level of the individual business unit. But the companies consist, in general, of multiple business units or operations. The corporate strategy defines how to integrate the strategies of the individual business units to create the synergies that the units that operate independently of each other lack.

The corporate strategy is described by a strategic map that identifies the specific sources of the synergies. Then, managers unfold this map vertically to the business units, whose strategic maps can then reflect the objectives related to their local strategies and the objectives that are integrated into the corporate strategy and the strategies of other business units.

2. How do we align the support units with the strategies of the business unit and the corporate strategy? Executives tend to treat support units and the functions of corporate personnel as a discretionary spending center, that is, as overhead departments whose objective is to minimize operating expenses. As a result, the strategies and operations of the support units do not align well with those of the company and the business units they are supposed to support.

Successful execution of the strategy requires support units to align their strategies with the value creating strategies of the company and its business units. The support units should negotiate service level agreements with the business units to define the set of services they will provide. The creation of strategic maps and BSC of the support units, based on the service level agreements, allow each unit to define and execute a strategy that improves the strategies that the business units are implementing.

3. How do we motivate employees to help us execute the strategy? Ultimately, employees are those who improve processes and execute the projects, programs and initiatives required by the strategy. They must know and understand it to successfully relate their daily operations to the strategy. Formal communication programs help employees understand the strategy and motivate them to achieve it.

Managers strengthen the communication program by aligning personal goals and employee incentives with strategic corporate objectives and business units. In addition, training and professional development programs help staff achieve the skills they need for a successful execution of the strategy.

Operations Planning

How do companies integrate the long-term strategy into daily operations? Through an operational plan, focused on answering two key questions:

- What improvements to the processes are most critical to execute the strategy? The objectives of the process perspective of the strategic map represent the way in which the strategy will be executed. The strategic themes of the map originate in these key processes. For example, the strategic theme “Growing through innovation” requires an outstanding performance of the process of developing new products, while the theme “Forging a better loyalty in target customers” requires superior customer management processes.Some improvements to the processes are designed to meet the objectives of cost reduction and greater productivity of the financial perspective, while others are focused on excelling in the social and regulatory objectives. These process improvements, different from the short-term strategic initiatives developed in Stage 2, represent improvements to existing processes.Companies must focus their total quality management, six sigma and reengineering programs on improving the performance of the processes directly related to the strategic objectives that will generate the desired improvements in the client’s objectives and the strategy’s financial objectives. The customized control panels, integrated by key indicators of the performance of local processes, provide focus and feedback to the efforts of improvements to the processes of the employees.

- How do we relate the strategy with the operational plans and budgets?: The improvement plans to the processes and the high-level goals and strategic indicators of the BSC must become an annual operating plan. This plan has three components: a detailed projection of sales, a plan of resource capacity and the budgets of operating expenses and capital expenditures.

- Sales projection: organizations must translate their revenue goals from the strategic plan into sales forecast. The “beyond budgeting” movement holds that companies respond continuously to their dynamic environments by rethinking their quarterly sales for the next five or six quarters.Whether it is an annual or quarterly plan, any operating plan is launched based on a sales projection, a task that is facilitated by analytical approaches (driver-based planning). To provide the level of detail necessary for the operating plan, the sales forecast should incorporate the quantity, mix, and nature expected from individual sales orders, production runs, and transactions.

- Resource capacity plan: companies can use a cost model based on activities and driven (or addressed) by time (TDABC) to translate detailed sales projections into estimates of resource capacity needed for forecast periods. The cost system based on activities (ABC) is a tool capable of measuring the costs and profitability of processes, products, customers, channels, regions and business units. But its “killer application” is the planning and budgeting of resources.Since the TDABC model uses capacity impellers, in general time, to relate in a map the coverages with the transactions, the products and the clients managed by each process, it is possible to graph in a simple way the sales projections and the improvements to the processes and relate them to the amount of resources (people, equipment and facilities) necessary to comply with the plan.

- Dynamic operating and capital budgets: once the managers agreed on the amount and mix of resources needed for a future period, they can easily calculate the financial implications of these resource commitments. The company knows the cost of the provision of each unit of resources.Multiply the cost of each type of resource by the amount of resources authorized and obtain the budgeted cost of providing that resource capacity for the operational and sales plan.Most of this capacity is represented by personnel costs and should be included in the operating expenses budget (OPEX). Increases in the capacity of equipment resources would be reflected in the capital budget (CAPEX). The outputs of this process are dynamic operating and capital budgets obtained quickly and analytically from the operating and sales plans.